Private Clients

Helping you discover more with your time through bespoke wealth management

Some of the products listed on our website may not be available in certain regions due to regulatory reasons. Please contact our local offices to speak to a qualified financial advisor.

By continuing to the website I accept the cookie policy

Helping you discover more with your time through bespoke wealth management

Collaborating with you to bring your vision to life

Unlock a variety of resources from our thought leaders, and come one step closer to your goals and aspirations.

Friday, March 03, 2023

Written By

Succession | Intergenerational Wealth Transfer | Tax Planning | Financial Advice

Share:

Much like most of the public has yet to create a will, most entrepreneurs have no succession plan in place. This might be because they have no family or because they don’t know where to start. But, often, it comes from the perception that succession planning is reserved only for high-net-worth individuals.

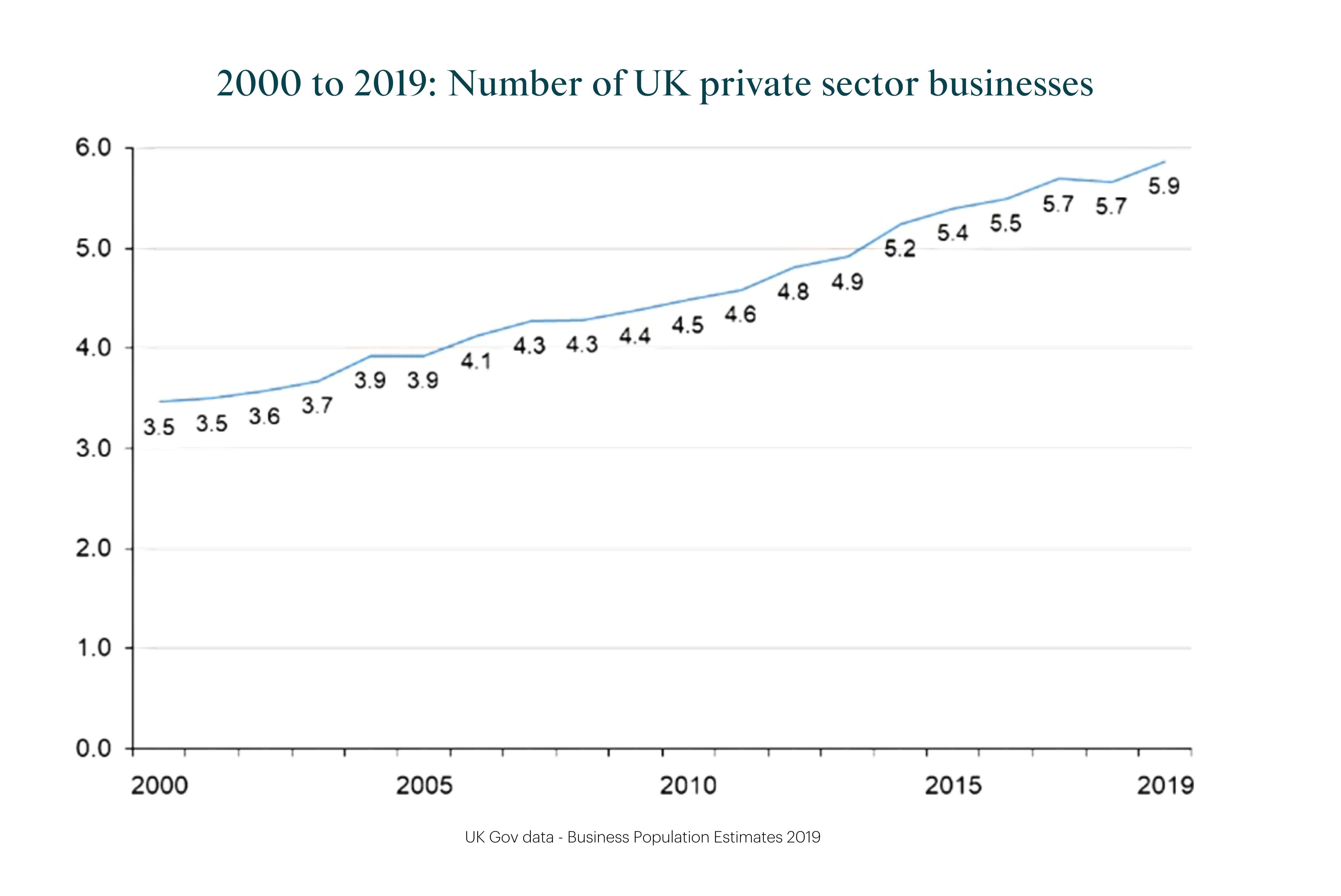

A 1980s study on manufacturing companies in the US showed that only a third of family businesses make it through the entire second generation, whilst only 13% survive the third. This is particularly concerning when 90% of businesses in the US are family owned (either passed down or concurrently run by relatives). This number is less in the UK, but it’s still the majority in most countries around the world.

A big threat to a business’s longevity is when the owner is not thinking in terms of decades, but rather year-on-year performance. The uncertainty of having no clear plan in place can lead to disruption among employees, a reduced valuation, legal issues, and family conflict.

But, things get even more tricky when looking at the modern-day entrepreneur. Entrepreneurs are deviating from traditional family business structures, bringing even more challenges. For example, consider the remote running of a letterbox media agency from abroad. Does anybody take over? How is this asset passed on to overseas families? This makes succession planning a little more elusive in a time when estate planning has never been so important.

When a business gets to a certain size, there are forces in place that can ensure its own survival. Stakeholder expectations, shareholder meetings, and the separation of ownership and control can offer some self-correcting guidance to high-net-worth individuals - be it as a founder or shareholder.

But, smaller business owners are very much on their own. With more control boiled down to fewer individuals, succession planning becomes all the more important. And, when the second generation doesn’t get a chance to take over in 70% of cases, this is clearly an area of neglect.

Of course, succession planning doesn’t have to be about passing a business on to relatives. When committing to proper succession planning, it may be apparent that no relative is appropriate or shares the same vision.

Estate planning is about consolidating your assets and identifying the beneficiaries. And, succession planning shouldn’t be viewed any differently.

It’s evident that the chances of a business’s survival are reduced with poor succession planning. Here are some possible reasons why.

The ultimate goal of succession planning is for the transition of passing on the business to be as smooth as possible.

No matter what stage of the business you are in, it’s never too late to begin. In fact, the longer the time frame of the plan, the smoother the transition will be. More importantly, this is a process that all business owners need to consider, not just owners of large firms and estates.

One of the biggest reasons for having no plan is that the owner doesn’t know where to start. This highlights the importance of speaking to an adviser early on and the legal complexities they can navigate through.

A succession planning adviser can objectively assess the business and its leadership. There are immediate benefits to yield here too, such as finding gaps in leadership and areas of improvement.

From here, you will work with an adviser to identify potential successors. This means assessing the skills, experience, potential, and vision of potential candidates. Then, a transitionary plan is made with legal and financial considerations and developing personnel accordingly. Compliance, taxation, and efficient estate planning are where an adviser shows their worth.

Neba Private Clients is licensed to operate in multiple regions. Neba Insurance Brokerage is registered with the Central Bank of UAE; Neba Private Clients is licensed by the Securities and Commodities Authority (SCA) UAE; NEBA Financial Solutions Ltd is registered with the Labuan Financial Services Authority (LFSA); Neba Private Clients Wealth South Africa (PTY) Ltd. authorised by the FSCA.

2024 Neba Private Clients. All rights reserved

Terms & Condition | Privacy Policy

Designed & developed by  by NEBA

by NEBA

For better web experience, please use the website in portrait mode

Financial Analyst

Financial Analyst